Quarter-End Chaos Meets Rising OI — mTLP Holds Its Ground Against Macro Headwinds

TL;DR

- Global risk-off intensified on Iran conflict escalation and stagflation fears; BTC briefly touched ~$74k mid-week before collapsing to close the week near ~$66k following the $14.16B quarterly options expiry — the largest of 2026; SOL and SUI each declined ~-5%

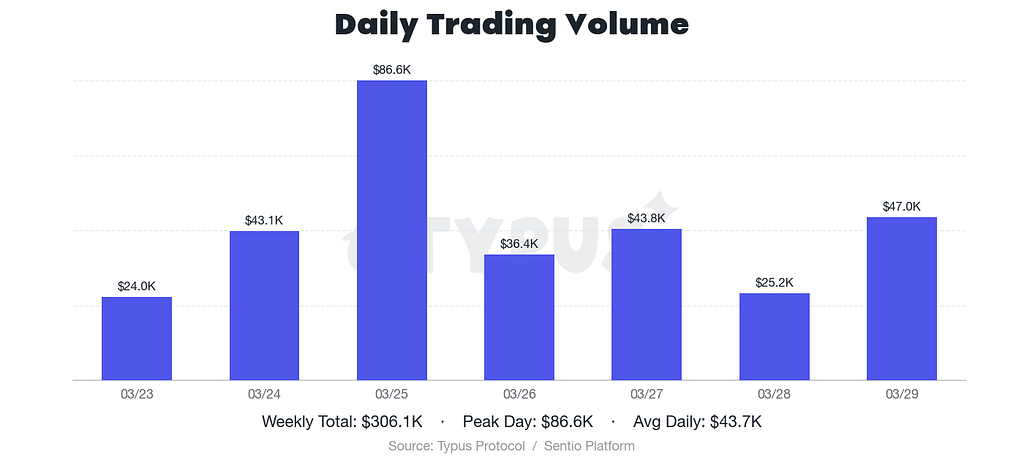

- Platform volume reached ~$305k (-19% WoW), a second consecutive weekly decline, as macro uncertainty and post-expiry repositioning weighed on activity; BTC dominated at ~48% of notional

- mTLP returned -1.02%, slightly trailing the basket return of ~-0.64%; strategy contributions from fees and counterparty activity remained positive while SUI’s decline exerted the primary drag through basket exposure

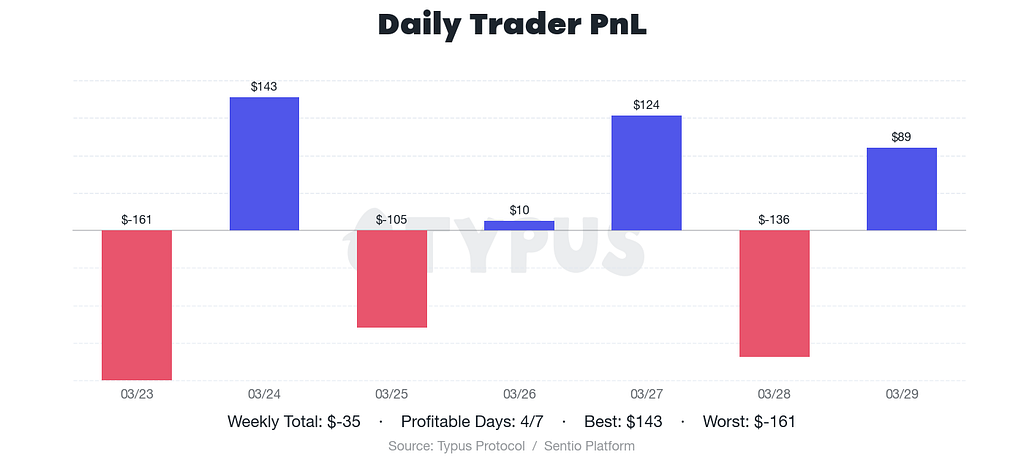

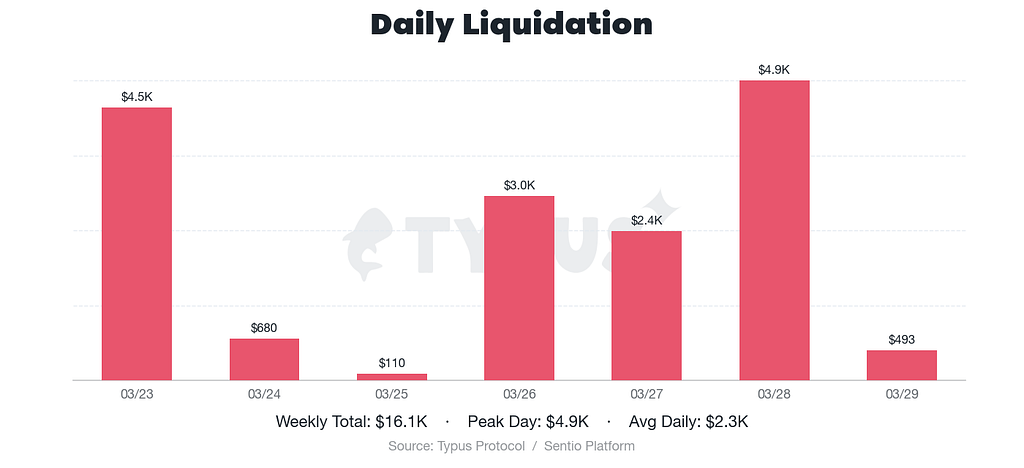

- Traders finished the week near breakeven at ~-$35 in net realized PnL; ~$16k in liquidations — concentrated around Monday and Saturday sell-off sessions — flowed into the pool as counterparty gains

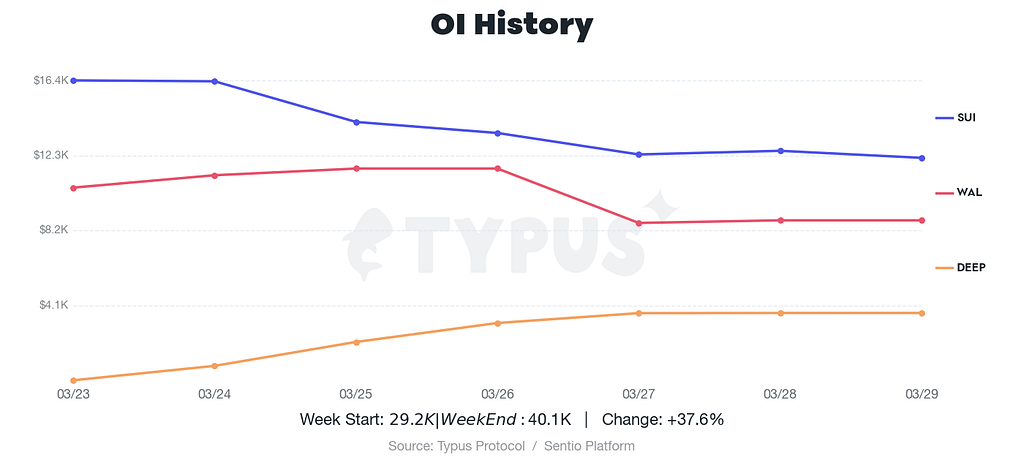

- Open interest surged +50% WoW to ~$40k despite falling prices, led by aggressive SUI and BTC long positioning — signaling traders are positioning ahead rather than retreating

Quarterly Expiry Triggers Sell-Off as Macro Pressure Builds

Macro drove the week from start to finish. Escalating tensions — including a 48-hour ultimatum to Iran, force majeure declarations in Iraqi oilfields, and drone strikes on Kuwaiti refineries — sent Brent crude surging ~9% above $112/barrel. The Fed held rates at 3.50–3.75% with a hawkish dot plot (14/19 participants projecting no cut or only one cut for 2026), cementing the stagflation narrative that has defined the quarter.

Markets followed a familiar arc: assets rallied Monday through Wednesday, with BTC briefly touching ~$74k mid-week, before the $14.16B quarterly options expiry on March 27–2026’s largest — triggered a sharp reversal. BTC fell to as low as ~$65,720 in the 24 hours following settlement, closing the week near ~$66k. SOL and SUI each shed ~-5%, the latter more sensitive to the risk-off positioning that dominated Friday and the weekend. The Fear & Greed Index closed at Extreme Fear (12–13), extending a 46+ day streak — the longest since mid-2022.

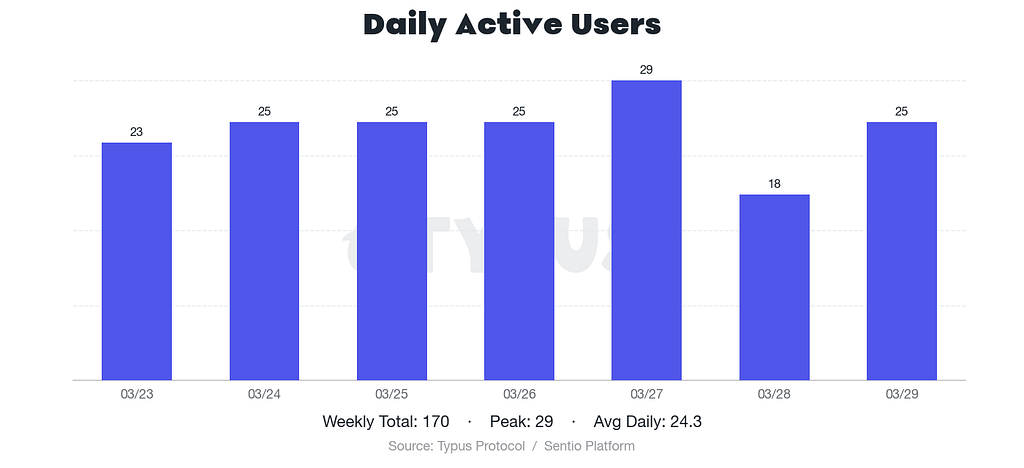

Against this backdrop, weekly volume on Typus adjusted to ~$305k — cooling ~-19% from the prior week and marking a second consecutive weekly decline. BTC led volume at ~48% of notional, followed by SUI at ~32%. Daily active users held steady throughout the week with a brief uptick heading into the expiry event.

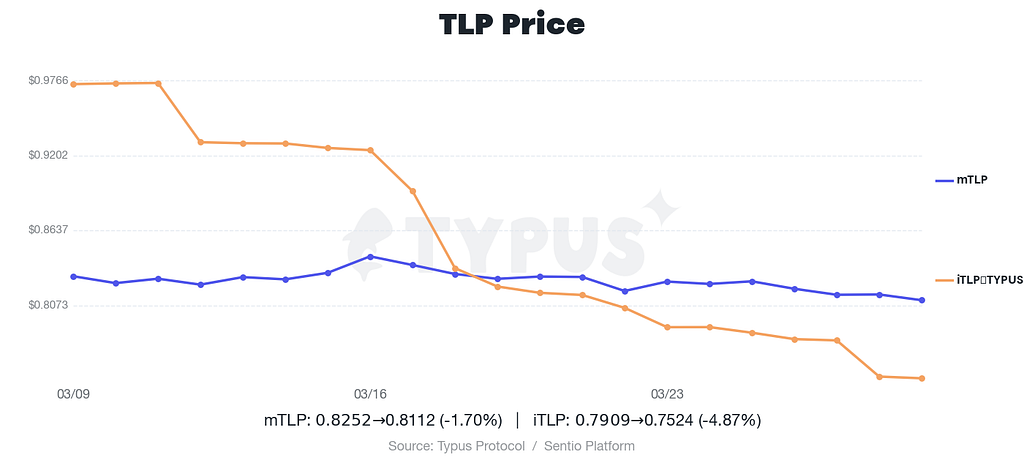

Strategy Returns Stay Positive as Basket Drag Weighs on mTLP

mTLP’s -1.02% return this week requires context. The basket return — driven by SUI’s ~-5.5% decline weighted at 11.5% of the pool — accounted for roughly -0.64% of that move. The remaining ~-0.38% reflects a mild alpha miss, though strategy-level contributions from fee income and counterparty gains remained positive throughout. Put differently: the LP mechanism did its job; it was directional market exposure, not strategy mechanics, that drove the week’s outcome.

The 11.5% SUI weighting in mTLP is worth highlighting. With ~88.5% of the pool in USDC, even a sharp -5.5% SUI decline translates to only ~-0.64% of basket drag — a structural buffer that mTLP’s USDC-heavy composition provides relative to a pure SUI hold.

iTLP-TYPUS posted -6.60% for the week. The pool’s smaller size amplifies sensitivity to funding cost swings and directional positioning in the TYPUS market; the magnitude this week reflects that structural volatility. As a pure USDC product, iTLP’s returns are driven entirely by fee income and counterparty outcomes — the -6.60% points to an adverse week on that axis rather than any underlying asset exposure.

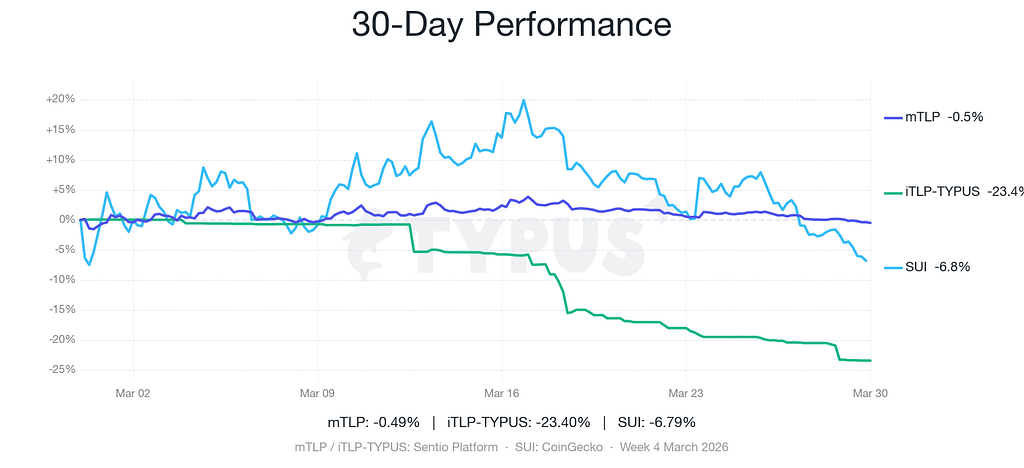

TLP vs. SUI: A 30-Day Performance Deep Dive

Across all four weeks of March 2026, mTLP returned -0.10% on a compounded basis — outperforming SUI’s -3.12% decline over the same period. The monthly picture reflects mTLP’s structural role: capturing fee income and counterparty gains while limiting net directional exposure to SUI price swings through USDC weighting.

iTLP-TYPUS returned -23.44% over the 30-day window, reflecting a period of elevated funding costs and unfavorable directional outcomes in TYPUS positioning. With all three assets negative across the month, risk-adjusted return metrics are omitted — negative Sharpe ratios carry limited interpretive value in this context.

Traders Navigate the Expiry Whipsaw Near Breakeven

Traders finished the week with ~-$35 in net realized PnL — effectively breakeven against a highly volatile backdrop. The week’s pattern mirrored the macro arc: Monday opened with losses as the sell-off hit early, Tuesday and Wednesday recovered, and Friday through the weekend saw renewed pressure as post-expiry momentum carried through.

Liquidations totaled ~$16k, with the heaviest events clustering on Monday (~$4.5k) and Saturday (~$4.9k) — both days of sharp directional moves tied to Iran conflict news flow. The pattern suggests traders were repeatedly caught off-sides during rapid headline-driven reversals. From a counterparty perspective, the ~$16k in liquidation proceeds contributed to LP income, offering a modest offset against the basket drag.

Open Interest Surges +50% Into the Sell-Off — Positioning for Recovery

The week’s most striking divergence: while price fell and volume declined, open interest expanded sharply — rising ~+50% from ~$26.8k at week-open to ~$40.1k by Sunday. When OI rises against falling prices, it typically signals fresh long positioning rather than short-covering — traders building into weakness rather than exiting it.

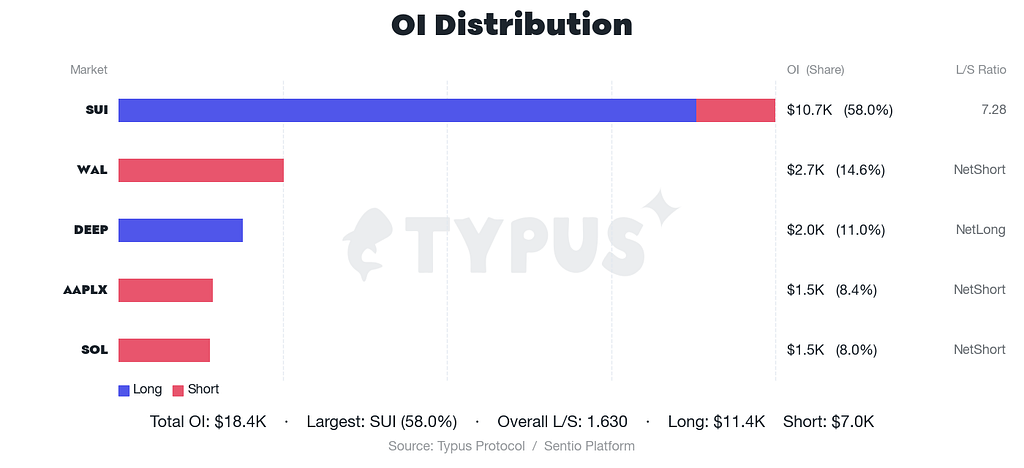

SUI led the build, with its open interest more than doubling over the week to claim ~48% of total platform OI. BTC positions also expanded materially, with the aggregate L/S ratio settling near 1.50 — a moderately long-biased posture. The OI expansion into a macro sell-off week reads as a forward-looking bet: participants appear to be front-running a recovery rather than responding to current conditions.

March 2026 closed on a familiar tension: macro uncertainty pressing prices lower while on-chain conviction quietly built from beneath. mTLP tracked near-basket returns across the month, preserving capital against SUI volatility while the LP mechanism continued generating positive strategy contributions. The sharp OI expansion into the quarterly expiry week — with traders adding longs even as BTC fell from $74k to the low $60s — suggests the market is positioning ahead, not retreating. With Iran developments, US NFP, and March CPI all due in the coming week, April’s opening act may be the catalyst that resolves this divergence.

Earn real yield: https://typus.finance/tlp/

Follow us: https://x.com/TypusFinance

【免责声明】市场有风险,投资需谨慎。本文不构成投资建议,用户应考虑本文中的任何意见、观点或结论是否符合其特定状况。据此投资,责任自负。