TL;DR

- Strong earnings from major technology firms supported weekly gains in both the S&P 500 and the Nasdaq, despite continued weakness in the industrial sector.

- Resilient economic data and expectations of a “higher-for-longer” Federal Reserve policy stance pushed the 10-year U.S. Treasury yield to 4.31%.

- Crypto markets rebounded over the past week, led by a 6.6% increase in BTC alongside $823.7M in spot BTC ETF inflows. ETH also advanced 4.7%, supported by $155M in ETF inflows.

- STRC remained under pressure, trading below its US$100 par value despite $846M in total volume. The upcoming April 28 vote on semi-monthly distributions may reduce dividend-driven volatility and support a move closer to par.

- The Governor of the Bank of Korea expressed support for CBDCs and tokenized deposits, while advancing the pilot phase of Project Hangang.

- JPYC raised $17.62M in a Series B extension to scale its yen-denominated stablecoin infrastructure and ecosystem integrations.

- 3F raised $4M in a seed round to bring leveraged RWA carry strategies on-chain.

Macro Overview

S&P 500 and Nasdaq Rise on Tech Earnings While Dow Lags, PMI and Labor Data Exceed Expectations, Showing Economic Resilience

US equity markets showed mixed performance during the week. The S&P 500 gained 0.79%, closing at 7,165.08, and the Nasdaq Composite surged 1.77% to 24,836.60, boosted by strong quarterly earnings from mega-cap technology companies. In contrast, the Dow Jones Industrial Average slipped 0.43% to end at 49,230.71, weighed down by the industrial and energy sectors. The market sentiment remained fragile as investors balanced optimistic corporate guidance against ongoing geopolitical tensions in the Middle East and a resilient labor market, suggesting the Federal Reserve may maintain higher interest rates for longer. Technology stocks continue to be the primary driver of the broader market indices, while traditional industrial sectors face headwinds from elevated energy costs and global supply chain realignments.

The energy sector remained a focal point of volatility as the US-Iran conflict continues to impact global supply expectations. WTI crude oil prices fluctuated as reports emerged of potential diplomatic breakthroughs mediated by Oman and Qatar. The US indicated that while military readiness remains high, there is a path toward de-escalation if the Strait of Hormuz is fully reopened for international commerce. However, the energy market remains on edge, with any signs of stalled negotiations leading to immediate price spikes. The impact of sustained high energy prices is beginning to manifest in broader inflationary pressures, complicating the Federal Reserve’s mission to return inflation to its 2% target.

Recent economic indicators released during the week pointed to continued resilience in the US economy. The Flash Composite PMI remained in expansionary territory, suggesting that despite high borrowing costs, the services and manufacturing sectors are holding up. Weekly jobless claims came in lower than anticipated, underscoring the tightness of the labor market. This economic strength, while positive for growth, has led to a recalibration of interest rate expectations. Markets are now pricing in a higher probability that the Federal Reserve will delay any potential rate cuts until late 2026 or even 2027. The “higher for longer” narrative has gained traction, contributing to the upward pressure on Treasury yields seen throughout the week.

Asian equity markets faced a challenging week as regional investors weighed the impact of the US-Iran war on energy-importing economies. Japan’s Nikkei 225 and Hong Kong’s Hang Seng Index saw increased volatility. The Bank of Japan (BOJ) maintained its ultra-loose monetary policy but signaled growing concern over imported inflation driven by the weak Yen and high oil prices. The interdependence of Asian supply chains makes the region particularly vulnerable to any further disruptions in the Middle East.

Looking ahead, investors will closely monitor the continuation of the tech earnings season for further clarity on sectoral momentum and margin trajectories in a higher-rate environment. Geopolitically, any concrete progress or setbacks in U.S.-Iran diplomatic channels could significantly impact risk sentiment. Investors will remain alert to news flow for indications of de-escalation or renewed tensions that could drive volatility. Any additional PMI releases and labor market reports will be key to confirming the durability of the current expansion phase. Inflation metrics will also be scrutinized for signs of moderation that could influence expectations for Fed policy. (1)

The US Dollar Index edged higher to 98.51 this week as strong economic data and rising Treasury yields supported the greenback. Safe-haven demand also persisted due to the ongoing Middle East conflict. (2)

Treasury yields edged higher as the market priced in a more hawkish Federal Reserve path. Strong PMI and labor data reinforced the view that the economy can withstand current rate levels. (3)

Gold prices retreated to 4,708.62 from recent highs as rising yields and a stronger dollar increased the opportunity cost of holding the metal. Profit-taking occurred following reports of potential diplomatic progress in the Middle East. (4)

Crypto Markets Overview

1. Main Assets

BTC rose 6.6% last week, while ETH gained 4.7%. Spot BTC ETFs recorded net inflows of US$823.7M, and spot ETH ETFs saw net inflows of US$155M. Meanwhile, the ETH/BTC ratio edged down slightly by 1.7%. (5)

Market sentiment also improved modestly from last week, with the Fear & Greed Index rising to 47, remaining in Neutral territory. (6)

2. Total Market Cap

Total crypto market cap rose 5.2% last week, while the market cap excluding BTC and ETH increased by 2.6%. Altcoin market cap excluding the top 10 also gained 3.7%, suggesting a modest broadening of risk appetite beyond major assets.

3. STRC Performance

STRC recorded $846M in trading volume last week, with all trades below its US$100 par value. This makes ATM issuance less attractive, as issuing below par could further pressure the price and create a negative feedback loop.

Historically, STRC often trades below par around ex-dividend dates, falling by about US$0.45 on average and taking roughly 12 days to recover.

A proposal to shift from monthly to semi-monthly payouts will be voted on April 28. If approved, smaller and more frequent distributions could help reduce dividend-driven volatility, keep STRC closer to par, and improve liquidity. (7)

Among Strategy’s financial instruments, STRC accounted for 85% of total trading volume, down from 93% the previous week. The next largest were SATA (Strategy’s variable-rate perpetual preferred stock) at 7.1% and STRK (Convertible perpetual preferred stock) at 3.6%.

Last week, Strategy purchased 34,164 BTC at an average price of approximately $74,400, bringing its total Bitcoin holdings to 815,061 BTC.

4. Top 30 Crypto Assets Performance

Among the top 30 assets, prices surged 4.2% on average, Memecore, ZCash, and XMR led the gain.

The Key Crypto Highlights

1. Coinbase launches crypto-backed USDC loans in the UK as FCA advances regulatory framework

Coinbase has rolled out crypto-backed USDC loans for UK users, allowing borrowing against BTC, ETH and cbETH via the Morpho lending protocol on Base, with loan sizes reaching up to $5 million depending on collateral levels and market-based variable rates. The launch expands Coinbase’s onchain lending suite beyond the US and comes as the UK’s Financial Conduct Authority (FCA) consults on a comprehensive crypto regime expected by October 2027, covering stablecoins, trading platforms, custody and staking. (8)

2. Bank of Korea governor endorses CBDCs and tokenized deposits while advancing Project Hangang pilot

Bank of Korea reaffirmed support for wholesale CBDCs and tokenized deposits, confirming progress into Phase 2 of the Project Hangang blockchain settlement pilot and continued participation in the BIS-led Agora cross-border tokenization initiative. Notably, stablecoins were absent from the policy outlook despite ongoing domestic debate over won-pegged issuance rules, while South Korea’s finance ministry separately plans a 2026 pilot using tokenized deposits for selected government expenditures, signaling a preference for bank-based digital money rails over private stablecoin alternatives in the country’s evolving digital payments strategy. (9)

3. Thailand SEC proposes allowing crypto firms to offer derivatives within existing licenses

Thailand’s Securities and Exchange Commission (SEC) is consulting on rule changes that would allow licensed digital asset firms to apply directly for derivatives licenses without establishing separate entities, lowering barriers to entry while strengthening oversight and conflict-of-interest controls. The proposal builds on earlier recognition of digital assets as eligible futures underlyings and aims to expand investor hedging tools while aligning Thailand’s derivatives framework with international standards, with public feedback open until May 20. (10)

Key Ventures Deals

1. JPYC raises $17.62M in Series B extension to scale yen stablecoin infrastructure and ecosystem integrations

Japanese yen stablecoin issuer JPYC raised an additional $17.62M in a Series B second close backed by investors including Metaplanet, bringing total Series B funding to roughly $28.9M. The capital will support system development, hiring, stablecoin issuance and settlement infrastructure, and strategic growth initiatives. Partnerships with Sony Bank, LINE NEXT’s Unifi wallet, and cross-border payment deployments, including pilots in El Salvador, highlight JPYC’s strategy to position itself as a programmable yen settlement layer spanning Web3 payments, commerce, and emerging AI agent economies. (11)

2. KAIO raises $8M strategic round to build compliant RWA and cross-chain asset infrastructure

KAIO has raised $8 million in strategic funding, bringing total funding to $19 million, with participation from returning backers Laser Digital and Further Ventures alongside new investor Tether. The protocol focuses on giving accredited investors compliant access to DeFi through fiat and stablecoins, while building appchain infrastructure for cross-chain transfers of tokenized real-world assets such as securities and real estate. Tether’s participation could point to future stablecoin-related integrations, reinforcing KAIO’s role in the broader push to connect traditional assets with onchain liquidity. (12)

3. 3F raises $4M seed round to bring leveraged RWA carry trades onchain

3F has raised $4 million in seed funding led by Maven 11, with participation from F-Prime Capital, Metalayer, GSR, Susquehanna Crypto, Gate Ventures and others, to build infrastructure for leveraged exposure to tokenized real-world assets. Built on Morpho, 3F aims to solve a key RWA demand bottleneck by letting users build leveraged carry positions in a single settlement cycle, avoiding the slow manual looping process caused by T+1 or longer RWA settlement delays. Its private beta has opened with JAAA leveraged vaults, using institutional-grade assets tokenized by Centrifuge and sub-managed by Janus Henderson, positioning 3F as a leverage and distribution layer for onchain RWA issuers. (13)

Ventures Market Metrics

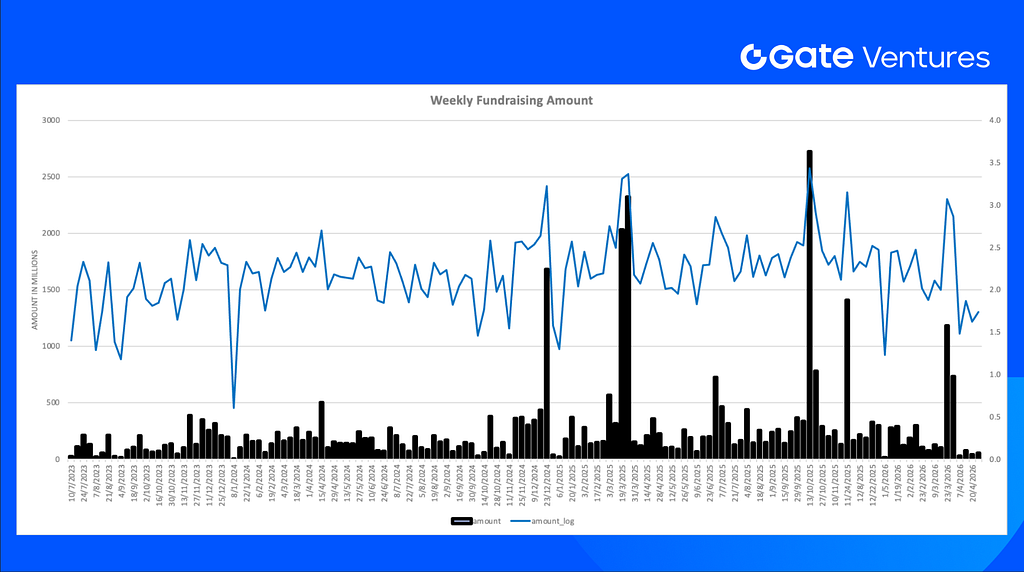

The number of deals closed in the previous week was 12, with Infra having 8 deals, Defi having 3 deals and Social having 1 deal.

The total amount of disclosed funding raised in the previous week was $54.89M, 1 deal in the previous week didn’t announce the raised amount. The top funding came from the DeFi sector with $29.62M. Most funded deals: JPYC ($17.62M).

Total weekly fundraising surged to $41.8M for the third week of Apr-2026, an increase of 31% compared to the week prior.

About Gate Ventures

Gate Ventures, the venture capital arm of Gate.com, is focused on investments in decentralized infrastructure, middleware, and applications that will reshape the world in the Web 3.0 age. Working with industry leaders across the globe, Gate Ventures helps promising teams and startups that possess the ideas and capabilities needed to redefine social and financial interactions.

Website | Twitter | Medium | LinkedIn

The content herein does not constitute any offer, solicitation, or recommendation. You should always seek independent professional advice before making any investment decisions. Please note that Gate Ventures may restrict or prohibit the use of all or a portion of the services from restricted locations. For more information, please read its applicable user agreement.

Reference:

- S&P Global Week Ahead Economic Preview, https://www.spglobal.com/market-intelligence/en/news-insights/research/2026/04/week-ahead-economic-preview-week-of-27-april-2026

- DXY Index, TradingView, https://www.tradingview.com/chart/z1UD772v/?symbol=TVC%3ADXY

- US 10 Year Bond Yield, TradingView, https://www.tradingview.com/chart/B9cgEklh/?symbol=TVC%3AUS10Y

- Gold Price, TradingView, https://www.tradingview.com/chart/z1UD772v/?symbol=TVC%3AGOLD

- BTC & ETH ETF Inflow: https://sosovalue.com/tc/assets/etf/us-btc-spot

- BTC Greed and Fear Index: https://alternative.me/crypto/fear-and-greed-index/

- Micro Strategy STRC Dashboard: https://bitcoinquant.co/company/MSTR

- Coinbase launches crypto-backed USDC loans in the UK as FCA advances regulatory framework, https://cointelegraph.com/news/coinbase-crypto-backed-usdc-loans-uk-morpho-fca-rules

- Bank of Korea governor endorses CBDCs and tokenized deposits while advancing Project Hangang pilot, https://cointelegraph.com/news/new-bank-of-korea-governor-backs-cbdcs-deposit-tokens-first-address

- Thailand SEC proposes allowing crypto firms to offer derivatives within existing licenses, https://asksurf.ai/pulse/en/kaio-strategic-funding-rwa-momentum

- JPYC raises $17.62M in Series B extension to scale yen stablecoin infrastructure and ecosystem integrations, https://www.nadanews.com/345497/

- KAIO raises $8M strategic round to build compliant RWA and cross-chain asset infrastructure, https://x.com/totalistrading/status/2043812703408664865

- 3F raises $4M seed round to bring leveraged RWA carry trades onchain, https://x.com/3f_xyz/status/2047385542644453404?s=20

【免责声明】市场有风险,投资需谨慎。本文不构成投资建议,用户应考虑本文中的任何意见、观点或结论是否符合其特定状况。据此投资,责任自负。