Fabius DeFi

Twitter

观点

Uniswap v4 Hook is one of the most interesting DeFi experiment rn 👀

The first wave obviously looks speculative. A lot of the attention came from fast-moving Hook-native plays, and most of them are probably not long-term assets.

But the reason I’m paying attention is simple:

liquidity is becoming programmable.

Over the past few weeks, Hook-native projects started pulling attention back to the Uniswap ecosystem.

> @sato_hub / $SATO crossed a $ 40M+ market cap.

> @uniqepv4 / $uPEG went from almost zero to over $30M in less than two weeks.

> SLONKS by @MichaelHirsch generated 1,200+ ETH in trading volume.

> @lo0pio / $LO0P started experimenting with AMM + lending.

> @flood_markets opened up the idea of routing pool reserves into yield.

At first glance, this feels like another degen rotation.

I think the more important signal is what these experiments reveal about Uniswap v4.

- V2 made AMMs simple

- V3 made liquidity more efficient

- V4 changes how liquidity behaves

Before v4, a pool was mostly passive. Traders swapped, LPs provided liquidity, and the pool followed fixed rules.

With v4 Hooks, developers can attach external logic directly to the lifecycle of a pool. That logic can run around swaps, liquidity changes, and other pool actions.

So a pool is no longer just a place where assets sit and wait for traders.

It can now have its own behavior.

A pool can support bonding curve launches, dynamic fees, limit orders, TWAMMs, LP automation, MEV-aware execution, NFT/game mechanics, yield-bearing reserves, or even lending markets inside the liquidity mechanism itself.

This is where the v4 architecture matters.

V4 uses a Singleton design, where pools live inside one unified contract instead of every pool needing a separate deployment.

It also uses flash accounting, where balance changes are tracked throughout a transaction and only settled at the end.

That makes complex routes, multi-hop swaps, LP adjustments, and Hook interactions more efficient.

Lower gas is useful, but cheaper execution is only the surface.

The deeper story is that Uniswap is becoming a permissionless AMM plugin layer.

> $SATO pumped because its tokenomics are embedded directly into the market mechanism.

- ETH goes into the Hook

- The Hook mints SATO through a bonding curve

- When users sell, tokens are burned and ETH is returned

- The mechanism itself becomes the product

This is different from the old token launch model.

Usually, a project launches a token, adds liquidity, then adds staking, buybacks, or incentives later.

With Hook-native assets, the order changes:

design market behavior first, attach liquidity second, then let every trade interact directly with that mechanism.

> $uPEG showed another side of the same idea.

It did not need the most complex financial design. It worked because it turned a Hook into a simple cultural object: Uniswap lore + JPEG culture + v4 mechanics.

A swap was no longer just a swap.

It could become an onchain object.

> SLONKS showed the NFT/game side with cheap minting, AI-style art, Hook mechanics, and a fast social feedback loop.

> $LO0P moved in a more DeFi-native direction.

The pool starts to look less like a simple swap venue and more like a system that combines an AMM with a credit market.

Users buy tokens along a curve, lock those tokens, and borrow ETH from the same system.

This is why the first wave of Hooks looks like memes.

Memes are the fastest way for a new primitive to become legible to the market.

But the design space underneath is much wider:

Dynamic fee markets

TWAMMs

LP automation

Limit orders

MEV-aware pools

Yield-bearing reserves

Hook-native lending

Liquidation auctions

NFT/game mechanics attached directly to liquidity

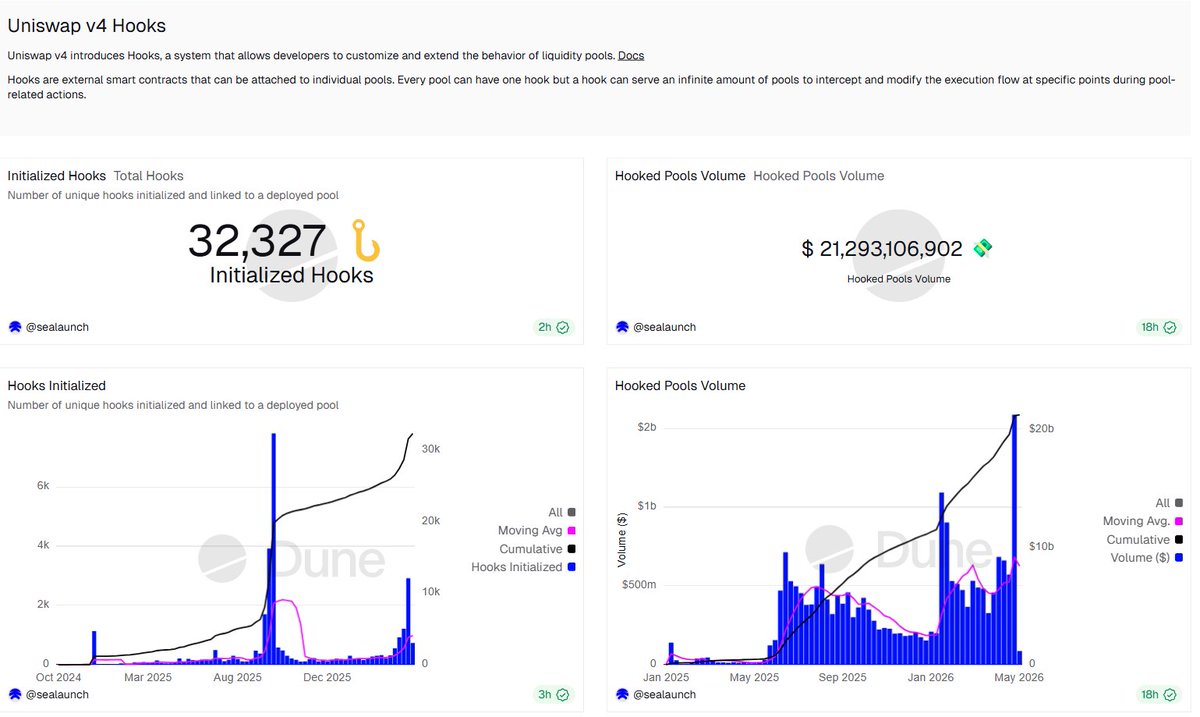

Public dashboards like Dune are already tracking Uniswap v4 activity across multiple chains, including TVL, fees, DEX volume, and hook pool data.

The numbers are still not perfect because certain hooked pool events can be under-reported or over-reported.

Still, directionally, the trend is clear:

developers are now experimenting directly at the liquidity layer.

That also changes how I would research these assets.

For normal tokens, people usually check supply, tax, owner, liquidity, holders, and unlocks.

For Hook-native assets, the mechanism matters just as much as the chart.

I would want to understand what the Hook controls, whether it takes custody of assets, whether fees can be withdrawn, whether admin controls exist, how reserves are accounted for, and what happens at terminal states.

In other words:

the mechanism is the edge, but it is also the attack surface.

Opportunity and risk sit in the same place here.

Most Hook tokens will probably die. There will be forks, attention games, broken designs, and one-rotation charts.

But the primitive itself is worth paying attention to.

Uniswap used to be mainly a swap venue.

With v4, it is expanding into programmable liquidity middleware.

Hook builders can borrow Uniswap’s settlement layer, router network, LP base, brand, and distribution, then add custom market behavior on top.

That is a much bigger shift than just a “new meme meta”.

The next DeFi primitive may not need to launch as a new L1, appchain, or standalone protocol.

It may start as a custom Uniswap v4 pool.

Pool = market

Hook = behavior

Liquidity = programmable state

That is why I’m paying attention to Hook Summer.

Not for every ticker, for the design space it opens up 💎